Since 2010, the Global Law Experts annual awards have been celebrating excellence, innovation and performance across the legal communities from around the world.

posted 2 hours ago

Introduction

Cameroon’s mobile money sector has experienced explosive growth, with platforms like MTN Mobile Money and Orange Money serving millions of users and driving financial inclusion across urban and rural areas. However, this rapid expansion has been accompanied by a surge in fraud, scams, and unauthorized transactions. Social engineering attacks, SIM swaps, phishing (including SMiShing), agent-driven fraud, and PIN-sharing schemes are increasingly common, resulting in significant financial losses for consumers and operators alike.

For fintech platforms operating as Payment Service Providers (PSPs) or Electronic Money Issuers (EMIs), these risks carry not only financial and reputational consequences but also serious regulatory and legal liabilities under CEMAC, BEAC, COBAC, and national frameworks.

Licensed PSPs and EMIs must implement robust Know Your Customer (KYC), transaction monitoring, and Suspicious Transaction Reporting (STR) systems. Failure to do so exposes operators to fines, license suspension, or revocation. Recent enforcement trends, including the 2026 push on licensing and dematerialization, signal heightened scrutiny.

Common Forms of Mobile Money Fraud in Cameroon

Fintech platforms frequently encounter:

These issues contribute to substantial economic losses, with cyber fraud (including mobile money scams) previously estimated at hundreds of millions CFA francs annually.

Key Legal Risks for Fintech Platforms

1. Civil Liability to Customers: Platforms may be held responsible for unauthorized transactions if they fail to demonstrate adequate security measures or prompt resolution of disputes. Consumer protection rules emphasize timely refunds and clear dispute mechanisms.

2. Regulatory Sanctions: Non-compliance with AML/KYC, cybersecurity, or interoperability requirements can lead to administrative penalties, mandatory audits, or operational restrictions by COBAC/BEAC.

3. Criminal Exposure: Facilitating (even unwittingly) money laundering or fraud through weak controls may trigger ANIF investigations or prosecutions under cybercrime laws.

4. Reputational and Contractual Risks: Partner banks, telecoms, and agents may seek indemnification. Interoperability agreements raise complex questions on liability allocation for failed or fraudulent transactions.

5. Data Protection and Privacy: Breaches involving customer data can violate electronic communications and consumer protection decrees.

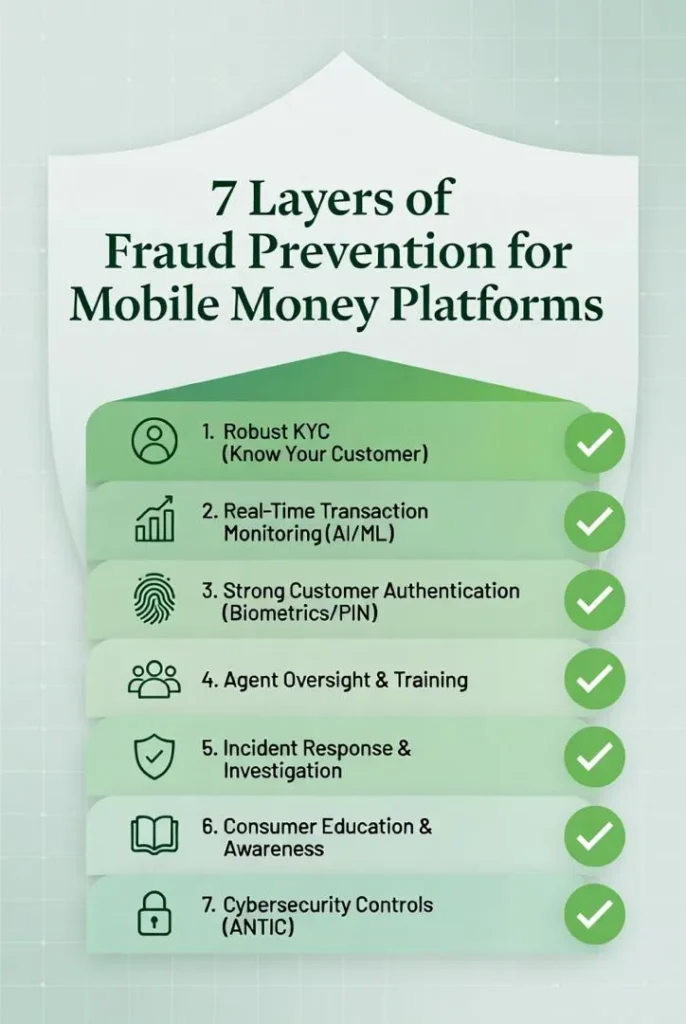

Best Practices and Compliance Strategies

To mitigate risks, fintech platforms should adopt a proactive, multi-layered approach:

Legal counsel plays a critical role in drafting policies, negotiating interoperability agreements, preparing license applications/amendments, and representing platforms in regulatory inquiries or disputes.

Recommendations for Fintech Operators

Author

No results available

posted 6 minutes ago

posted 1 hour ago

posted 2 hours ago

posted 2 hours ago

No results available

Find the right Legal Expert for your business

Sign up for the latest advisor briefings and news within Global Advisory Experts’ community, as well as a whole host of features, editorial and conference updates direct to your email inbox.

Naturally you can unsubscribe at any time.

Global Advisory Experts is dedicated to providing exceptional advisory services to clients around the world. With a vast network of highly skilled and experienced advisors, we are committed to delivering innovative and tailored solutions to meet the diverse needs of our clients in various jurisdictions.